Rate hike pause ‘will offer some relief to those struggling with housing costs’

Some homeowners may be breathing a sigh of relief after the Bank of England’s decision to press pause on interest rate hikes, but many are yet to fully feel the impact of the increases that have already taken place.

With many homeowners sitting on fixed-rate mortgages, the effects of previous rate rises are still working their way through, as people’s deals come to an end and they take out new deals at higher rates.

According to trade association UK Finance, around 800,000 fixed-rate mortgage deals are due to end in the second half of this year and 1.6 million are due to end next year.

Lucian Cook, head of residential research at estate agent Savills, said: “The Bank of England’s decision to maintain the current base rate is an important signal to the mortgage markets and should take some of the edge off the affordability pressures buyers are currently facing.

“However, a material improvement in mortgage affordability requires the prospect of a cut in interest rates coming on to the horizon. That still looks some way off, suggesting buyers’ budgets are going to remain constrained and that there is a little way to go before house prices bottom out.”

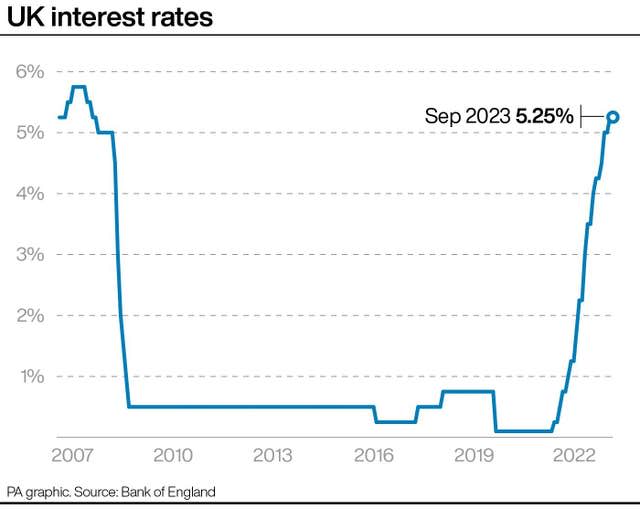

The pause follows 14 rises in a row, taking the base rate from 0.1% to 5.25%.

Earlier this week, consumer group Which? highlighted concerns around those who are due to come off fixed-rate deals around Christmas, a time when finances are often squeezed.

Average two-year fixed-rate mortgages are currently above 6%, according to data from financial information website Moneyfacts.

But Which? said that some of those who had previously fixed their deal in December 2021 could have got a rate below 2%.

Sam Richardson, deputy editor of Which? Money, said: “This latest decision may offer some relief for those around the country struggling with housing costs.

“However, Which? warned this week that around half a million homeowners are set to come off their fixed-term deals over the Christmas period, meaning households already under pressure due to the cost-of-living crisis could see their monthly repayments increase by hundreds of pounds.

“Those concerned about how they will repay their mortgage should contact their lender straight away – and doing so will not affect your credit score.

“Options may include extending the term of your mortgage, only paying the interest on your deal or taking a temporary payment holiday – and the most suitable will depend on individual circumstances. That’s why it’s crucial that lenders are available to help customers with appropriate and tailored support.”

People should bear in mind that extending the mortgage term or going interest-only for a period may mean that they end up paying more money to their lender in interest charges over the longer term.

Property professionals said the base rate pause could bring some “welcome reassurance” to the housing market.

Jeremy Leaf, a north London estate agent, said of Thursday’s rate pause: “Stability is so important to the property market and brings confidence to buyers and sellers sitting on the fence finding it difficult to budget before deciding to make their moves. This hold, after many months of rises, will bring some welcome reassurance.”

Riz Malik, director of Southend-on-Sea-based mortgage broker R3 Mortgages, said: “The markets should react positively, and we might witness even larger reductions in fixed rates.”

Gary Boakes, director of Salisbury-based mortgage broker Verve Financial, said: “We can finally breathe a sigh of relief after 14 straight base rate rises. This is truly fantastic news.”

Andrew Montlake, managing director of the UK-wide mortgage broker Coreco, said: “It now looks like we are at the very top of the interest rate cycle, with swap rates (which underpin mortgage pricing) continuing to ease and giving lenders more space to engage in a rate war as they battle for market share and look to get a good start to 2024.

“As this competition increases, we will see more products available starting with a four rather than a five and this will inevitably start to encourage more buyers back into the market as they seek to take advantage of the buyers’ market whilst it lasts.”

Nicholas Wilson, 66, who lives in Hastings in East Sussex, has seen his mortgage cost rise from about £440 per month last year to more than £900 now.

Mr Wilson was previously diagnosed with cancer and had asked followers on Twitter, now known as X, for financial assistance, though now his cancer is “undetectable” his fundraiser is inactive.

He told the PA news agency: “My followers raised enough money to pay my mortgage whilst I was having cancer treatment so I didn’t have to worry about my mortgage but that’s all finished now so every time there’s a rate increase my situation becomes more desperate.

“I wouldn’t be able to afford to buy anywhere else, I probably won’t be able to afford to rent, so I’ll probably end up in a caravan or something.”

Renters have been feeling the impacts of rent hikes, as higher mortgage rates feed through to them from landlords’ additional costs.

According to Office for National Statistics (ONS) figures released on Wednesday, private rental prices paid by tenants in the UK rose by 5.5% in the 12 months to August 2023, accelerating from 5.3% in the year to July 2023.

This was the biggest annual percentage change since the UK-wide records started in January 2016.

Meanwhile, savers have been making the most of jumps in cash savings rates as the base rate has increased.

Some providers have recently reported seeing significant rises in savers fixing into deals.

Ed Monk, associate director for personal investing at Fidelity International, said: “We know that more and more of our investing clients have been turning to cash as rates have risen, with money market and cash funds jumping to the top of Fidelity Personal Investing’s best-sellers lists this year.

“A pause in rate rises is further evidence that rates may have topped out and investors should understand the risks when they take shelter in cash. Rates on deposit accounts remain below inflation meaning a loss in real terms, while investors in cash may also be missing out on bigger – although less certain – gains from shares.”

Sarah Coles, head of personal finance at Hargreaves Lansdown, said of cash savings rates: “The very best deals may not be around for much longer. If you haven’t switched your easy access rate for some time, it’s also worth making a move while there are some really attractive rates on the market.

“However, this isn’t time to panic. If your current fixed-rate deal doesn’t come to an end for a while, don’t lose faith.

“The Bank of England’s insistence that the fight against inflation is ongoing means we could see more rises further down the line, and at the very least is likely to mean it keeps interest rates higher for a considerable period.

“It means that while we may see some of the most competitive rates retreat, we’re not expecting dramatic drops in the immediate future.”