Borrowing costs ‘might have peaked’ as Bank holds rates steady

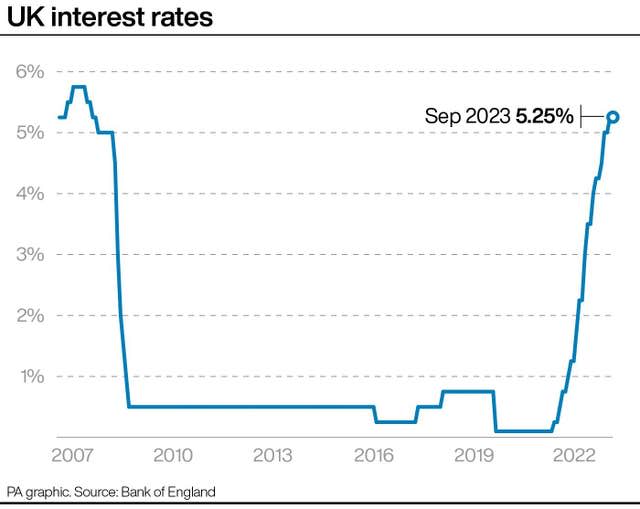

The Bank of England has kept its interest rate unchanged for the first time in almost two years, signalling that they might have finally reached a peak after a lengthy run of hikes that has battered borrowers.

Policymakers voted to hold rates at 5.25% after 14 increases in a row, although it was a close decision and they cautioned not to assume the end of rate rises.

They also said that the UK economy would grow slower than previously thought in the next few months.

Bank Governor Andrew Bailey left the door open to further rises in the future, promising to “take the decisions necessary” to return inflation to normal levels. Policymakers are next set to meet in November.

It is the first time since November 2021 that the Monetary Policy Committee (MPC) has met without deciding to raise interest rates.

Since then, the base rate was increased in 14 consecutive meetings, taking it from 0.1% to 5.25% as the Bank attempted to put a lid on runaway inflation.

Many had expected this week’s meeting to bring the 15th straight rise, and it almost did. Four of the nine-person MPC voted to raise rates to 5.5%.

Now some economists said that rates might not hit that level.

The pound fell in response to the rates decision, dropping 0.7% to 1.23 US dollars and was 0.5% lower at 1.15 euros.

Samuel Tombs, of Pantheon Macroeconomics, said he believes the Bank of England “probably is done” for now.

He said: “It’s not possible to confidently predict the outcome of the MPC’s final two meetings this year, given the marginal vote split this month and the committee’s deliberate attempts to keep its options open.

“Accordingly, we now think that 5.25% will be the peak level of bank rate in this hiking cycle.”

James Smith, an economist at Dutch bank ING, said the rate could start being cut by the middle of next year.

He added: “The risk is that the first move comes a bit later, but ultimately the UK economy can’t sustain rates above 5% indefinitely, and we think something closer to 3% is a more likely medium-term level.”

The MPC also downgraded its forecast for the UK’s economy on Thursday. It now expects gross domestic product (GDP) to rise just 0.1% in the third quarter of this year, compared with the 0.4% rise it forecast in August.

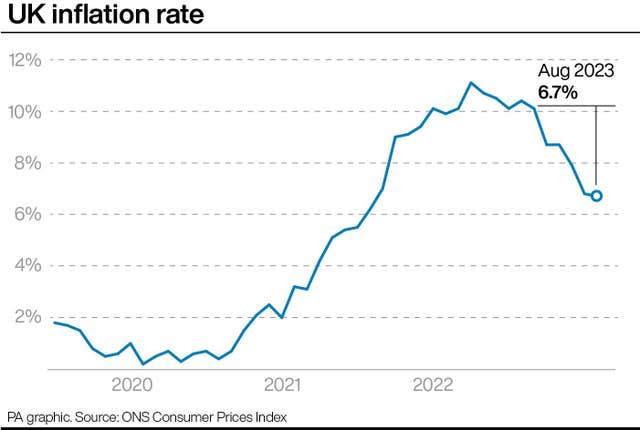

Speculation that the MPC might hold rates grew on Wednesday after the Office for National Statistics (ONS) revealed that consumer prices index (CPI) inflation rose less than expected last month.

The ONS said that inflation was 6.7% in August, down from 6.8% in July. The Bank itself had earlier forecast August inflation at 7.1%.

“Inflation has fallen a lot in recent months, and we think it will continue to do so,” said Mr Bailey, who voted to keep the rate unchanged.

“That’s welcome news. But there is no room for complacency. We need to be sure inflation returns to normal and we continue to take the decisions necessary to do just that.”

Economists who had expected a rise had speculated that decision makers would be convinced to hike further due to recent increases in wages.

MPC members, including Mr Bailey, have previously warned people against asking for too many pay rises as – they said – that could force inflation up even further.

But on Thursday the five that voted to keep rates unchanged said that “the recent acceleration in the AWE (average weekly earnings) was noteworthy but was not apparent in other measures of wages”.

They also noted that “headline and services CPI inflation had fallen back and were lower than had been expected”.

The four who voted to raise rates said that although there were some signs the economy was weakening, real household incomes had started to rise.

“These members judged that overall there was evidence of more persistent inflationary pressures,” the Bank said.

The MPC also voted unanimously to sell another £100 billion in Government bonds over the next 12 months, taking its holdings down to £658 billion.

Chancellor of the Exchequer Jeremy Hunt said: “We are starting to see the tide turn against high inflation, but we will continue to do what we can to help households struggling with mortgage payments.

“Now is the time to see the job through. We are on track to halve inflation this year and sticking to our plan is the only way to bring interest and mortgage rates down.”

The Bank’s decision follows in the footsteps of the US Federal Reserve, which on Wednesday evening revealed that it too had kept interest rates stable.